A central tenet of Labour’s plans for power during last year’s election was the ambition to ensure that Britain was supplied with clean power by 2030, with 95% of supply coming from clean sources. After achieving victory in the election, Labour has seen its plans for clean power move into motion. The Department for Energy Security and Net Zero (DESNZ) has founded the National Energy System Operator (NESO) to provide independent advice on the 2030 ambition and has since taken NESO’s advice and formulated its own 137-page action plan which can be found here. The overall conclusions were that the pathway toward clean power 2030 would require the following capacities:

- 43-50GW of offshore wind (currently 14.8GW)

- 27-29GW of onshore wind (currently 14.2GW)

- 45-47GW of solar power (currently 16.6GW)

- 23-27GW of short-duration energy storage (currently 4.5GW)

- 4-6GW of long-duration energy storage (currently 2.9GW)

- 2-7GW of flexibility technologies (currently 0GW)

- 80 network and enabling infrastructure projects

As the figures show, Labour will have to accelerate the UK’s renewable capacity at great speed to achieve its ambitions, effectively tripling capacity for some sources in just five years. It is for this reason that critics of the government believe the plans to be too ambitious and potentially damaging for the economy. For energy consumers, the question will be: how will this impact my energy costs?

Forecasts for Non-Commodity Costs:

To pay for the transition toward clean power 2030, the government will have to pass these costs on to consumers through their non-commodity charges. Non-commodity costs are charges all consumers pay for a variety of elements involved in delivery energy to consumers, this includes the generation of the energy, the transportation of the energy, maintenance and development of infrastructure and government-imposed levies.

Analysis by Npower Business Solutions suggests that clean power 2030 plans will have the biggest impact on the three following charges:

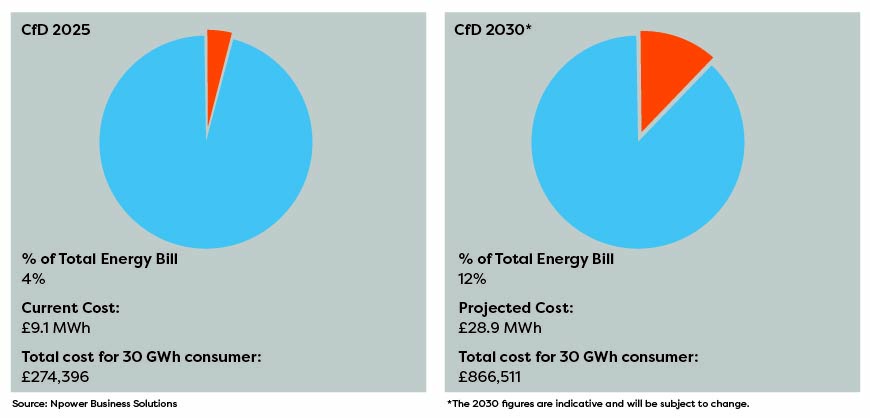

- Contracts for Difference (CfD)– A government levy, which is being used to fund clean power 2030 plans through auctions which provide the chance to invest in renewable projects.

- Transmission Network Use of Systems (TNUoS)– A system charge which covers the cost of installing and maintaining transmission systems, with the three UK transmission operators all expected to double investment as without this 2030 ambitions cannot be delivered.

- Balancing Services Use of System (BSUoS)- A daily charge for the energy that suppliers take from the National Grid, ensuring that the network grows at an adequate speed will be crucial to minimising increases to BSUoS charges.

As the above charts indicate, all three charges are forecast to rise significantly over the next five years, meaning it is becoming increasingly important to mitigate the impact through being proactive now and implementing effective energy management.

Handling Wholesale Costs:

Alongside the potential for rising non-commodity costs, the spotlight has also been placed on the UK’s commodity (wholesale) costs for its electricity, which are significantly high when placed in context with what other EU nations pay for their electricity. For 2025/26, commodity costs still make up 30% of your energy bill meaning they too can have a meaningful impact on your energy costs.

For experts the reason for the UK’s disparity is straightforward: it is due to the UK’s reliance on gas, the price of which was sent soaring following the Ukrainian invasion. Gas power plants set the market price for electricity, as on any given day the price of electricity is determined by the most expensive source of generation available which in the UK is gas. This means that electricity pricing is set by gas a staggering 98% of the time, this is compared to just 24% in Germany and just 7% in France.

Both France and Germany pay nearly half what the UK does per MWh of energy, with experts noting that a significant factor behind this is that they have both cut their reliance on gas. In France, nuclear energy contributes more than two-thirds of its electricity and in Germany renewables make up more than half its electricity. Combined with the fact that French and German energy bills also contain fewer non-commodity charges than the UK, businesses will be hoping that the UK government hits it target of reducing reliance on gas power stations to just 5% by 2030, allowing consumers to see tangible reductions in their energy bills.

How LGE can help:

LGE provides multiple services that can assist with minimising the increasing costs of commodity and non-commodity costs. These include:

- Bespoke procurement products that adopt agile strategies which stay on top of market movements and effectively manage risk. With markets currently in backwardation (meaning prices are cheaper further out rather than on the day ahead market) it is now a great time to take advantage of these conditions and implement trading strategies that will reduce commodity costs and off-set increasing non-commodity charges.

- Energy surveys which help improve energy efficiency and reduce wastage, in turn reducing consumption and the amount of non-commodity charges that will be paid.

- Feasibility studies for the installation of renewable technologies which include solar, wind, battery storage and small-modular reactors.

- Access to carefully selected partners for implementing these technologies and offering project management services for such work, with on-site self-generation not being subject to non-commodity charges.

For more information on these services speak to your account manager today or contact LGE at info@lgegroup.com.