With a ceasefire agreement between the United States and Iran now in place, LG Energy Group examines the state of global energy markets and infrastructure following four months of conflict that shook the foundations of global supply.

Market Prices:

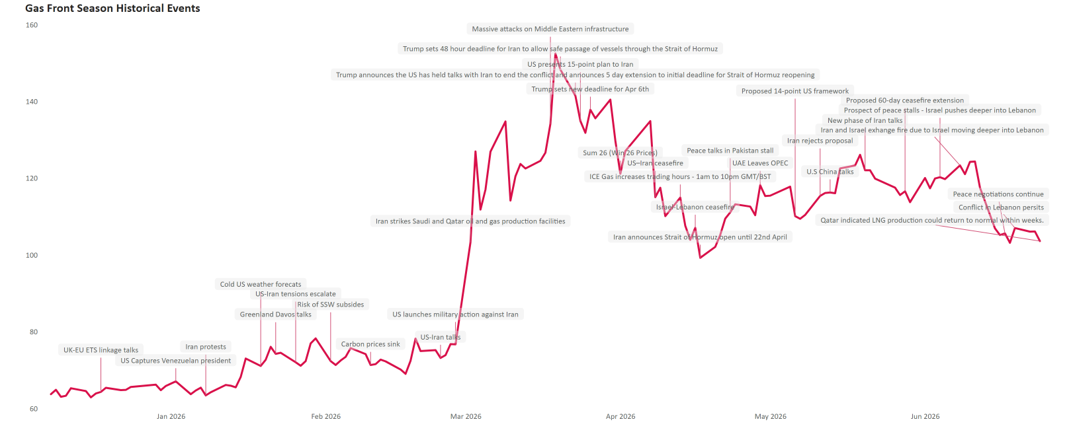

The effective closure of the Strait of Hormuz, a chokepoint through which approximately 20% of the world’s oil and gas flows, sent shockwaves through global energy markets. Between March and June, day-ahead NBP gas prices averaged 120.92p/th, a marked increase from the 90.35p/th recorded over the same period in 2025. Brent crude told a similarly stark story, averaging $102.00 per barrel across the period and briefly surging to $119.00 per barrel on 31st March, a level not seen since June 2022. The announcement of the peace deal did however trigger an immediate market response, with NBP gas falling back below 100.00p/th and Brent crude retreating sharply to $77.47 per barrel.

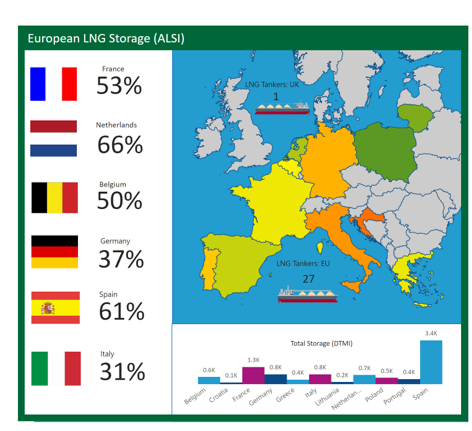

The easing of commodity prices will offer some relief to consumers already contending with rising non-commodity costs, though analysts caution against reading the dip as a return to pre-conflict prices. A sustained recovery in wholesale pricing hinges on several variables, not least the pace at which Qatar’s Ras Laffan LNG facility can be brought back to full operational capacity. Qatari authorities have confirmed that repair works are ongoing, with a target of returning to 80% capacity in the near term. Both the UK and European energy markets will be tracking progress at Ras Laffan closely, as the facility’s output will directly shape storage trajectory ahead of the winter season. Equally uncertain are the terms governing access to the Strait of Hormuz, which remain unresolved in the ceasefire framework, and the durability of the peace agreement itself.

Replenishing Storage Levels:

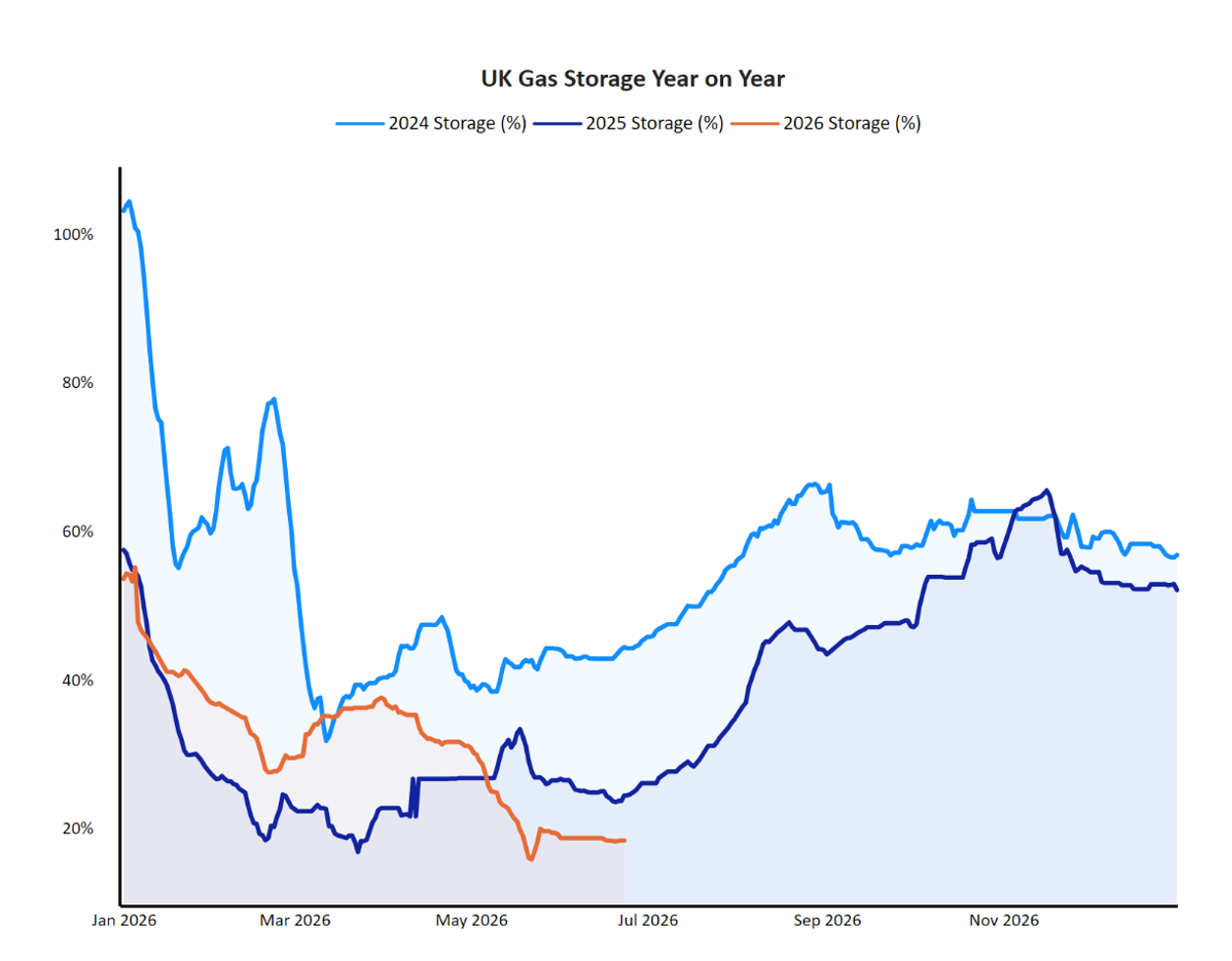

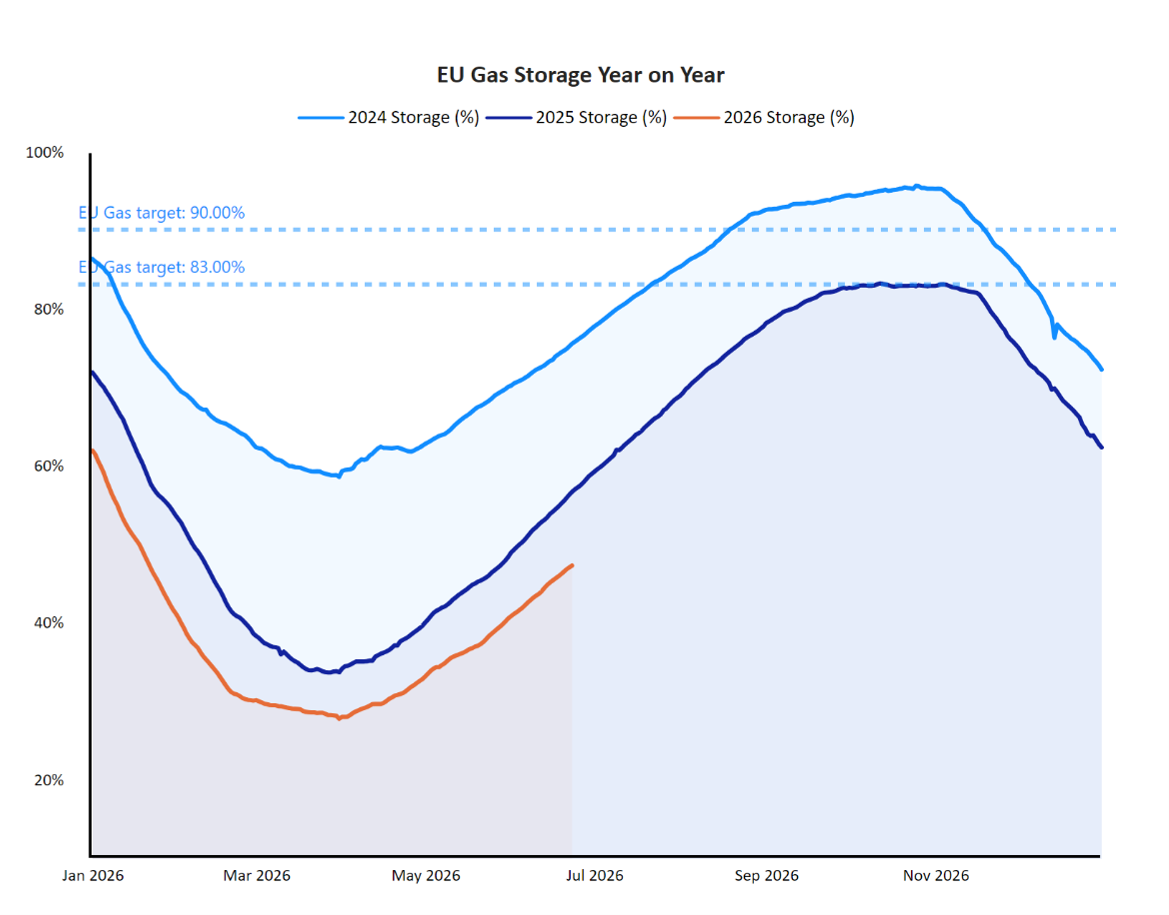

Even before the conflict began, gas storage had emerged as a pressure point. Competition for LNG cargoes between Asian and European buyers was already intensifying, a dynamic compounded by Europe’s ongoing shift away from Russian supplies. The conflict has deepened that rivalry at precisely the wrong moment, disrupting the summer injection season during which nations typically build stockpiles ahead of winter heating demand across the Northern Hemisphere. Looking ahead, several governments are now weighing options to bolster strategic reserves and revive idled production capacity as insurance against future supply shocks.

A further complication looms in the form of the El Niño weather pattern, which is forecast to bring warmer and drier conditions to Asia and Australia. Should this drive a significant uplift in Asian LNG demand through the summer and into autumn, European importers, including the UK, may find themselves in a competitive market, struggling to secure sufficient cargoes to meet winter storage targets.

The Future Outlook:

The long-term trajectory of energy costs will depend heavily on how further US-Iran negotiations unfold. In the near term, however, consumers are unlikely to see meaningful relief on their bills, with persistently elevated wholesale costs keeping inflation above target and monetary policymakers on edge. The Bank of England has held interest rates at 3.75%, acknowledging that while some of the conflict’s inflationary effects are already feeding through, the full extent of the disruption, across supply chains, infrastructure, and energy networks, remains deeply uncertain. Higher energy costs are expected to persist through the coming winter, underpinning what LG Energy Group characterises as a cautiously bullish outlook for wholesale markets. For the UK, the immediate challenge is navigating the intersection of below-average storage levels, incomplete infrastructure recovery and competition for LNG cargoes with Asian buyers. The long-term view also demands a structural rethink on greater supply diversification and more robust strategic reserves to form part of credible energy security framework.

Managing Flexibility:

Set against the backdrop of the 2022–2023 energy crisis, this latest conflict has sharpened UK businesses’ understanding of how rapidly geopolitical instability can unsettle markets and intensified the push for greater control over energy expenditure. The largest industrial and commercial consumers are already moving to explore flexibility mechanisms that can insulate them from wholesale price volatility. Those able to shift, reduce, or optimise their electricity consumption during periods of network constraint or price spikes stand to benefit on two fronts: reduced operational costs and increased revenue through participation in flexible energy markets. Solutions range from solar PV and battery storage to electrification and EV charging, technologies that can simultaneously reduce peak demand, maximise the value of on-site generation, support net zero commitments and unlock new revenue streams. Among the available mechanisms, the Demand Flexibility Service (DFS) offers businesses a structured route to earn revenue by shifting consumption away from peak periods, an increasingly attractive option for those seeking to optimise their energy assets in a volatile market environment.

How can LG Energy Group Help:

Through over a decade of experience, LG Energy Group has multiple solutions that can help large industrial and commercial consumers navigate volatility in energy markets. Our support includes:

- Proactive procurement strategies to stay ahead of market movements caused by geopolitical conflict and instability, helping to minimise increases to commodity costs

- Daily, weekly and monthly market intelligence services to ensure you know all that you need to know on developments in the market

- Strategies for reducing non-commodity costs, such as capacity reductions

- Feasibility studies for the installation of renewable solutions that will help engage in flexibility to reduce costs and increase revenue streams

- Access to renewable technology partners, with LG Energy Group handling the project management

Ultimately, the peace may hold and price may continue to soften, but for now, the market is not trading on peace alone, it is trading on proof: proof that Hormuz can remain open, proof that LNG capacity can return and proof that storage can be rebuilt before winter.