We are now three months into Cal24 and summer expiry is fast approaching, the seemingly colder periods have come and passed.

With the markets trending down steadily, seasonal UK energy prices are roughly at their lowest points since the highs of the energy crisis in August 2022, and with rates at the most attractive we have seen in a while it is time to look at those April starts.

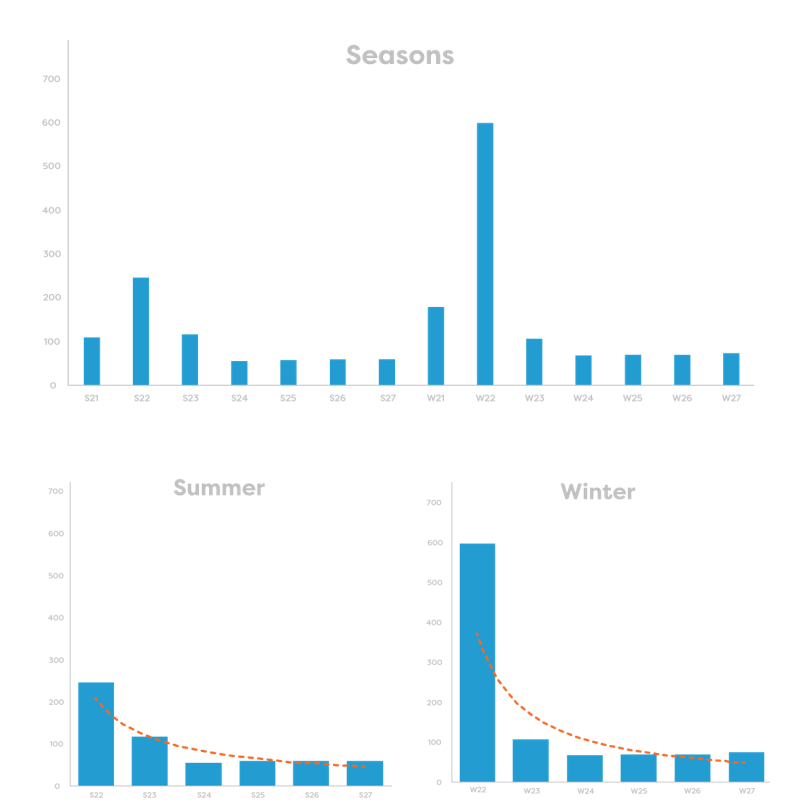

Locking in a mid-range flexible framework makes perfect sense right now, giving the optionality to purchase lower priced periods in the future and avoid those seasons that are currently seen as overpriced. The summer and winter periods of 2027 are currently the lowest priced seasons on the trading screens.

This wouldn’t be possible with fixed energy supply contracts, which would factor current risk scenarios into the rates and be set for the contract duration, not giving any chance to take advantage of falling markets.

Having had to navigate some near-term risk due to the cold snap that developed across the continent in early-to-mid February, UK gas storage is still recovering from spells of below average temperatures.

Going into the start of summer, caution is still required regarding global LNG supplies; cargoes are still avoiding the Red Sea like the plague, safe passage through the Suez Canal is not guaranteed and diversions are adding two weeks onto deliveries. The US has announced a temporary suspension to approvals for pending and future applications to export LNG from new projects. This has the East and most notably Japan, the world’s second largest LNG importer after China, concerned about supply.

Moreover, it is an election year here in the UK as well as the US; with energy security strategy high on all parties’ agendas much could change.